By Elias Brennan · Independent Cryptocurrency Payment Infrastructure & Cross-Border Settlement Analyst · May 2026 · 25 min read

Last updated: May 2026. This guide is updated quarterly to reflect changes in the fiat-to-crypto payment gateway landscape.

A fiat-to-crypto payment gateway is the bridge between the traditional card payment system and the blockchain. Your customer pays with their Visa, Mastercard, Apple Pay, or Google Pay — the same way they pay for anything else online. You, the merchant, receive the payment in USDC, USDT, Bitcoin, or another cryptocurrency directly to your wallet.

The customer’s experience is identical to any standard online purchase: a clean card payment form, a confirmation screen, a charge on their statement. They never interact with cryptocurrency. They don’t need a wallet, don’t need to understand blockchain, and don’t need to know you’re receiving crypto.

Your experience is fundamentally different from traditional payment processing: settlement in minutes instead of 3–7 business days. No rolling reserves. No fund freezes. No processor holding your revenue. Fees of 1–3% instead of 3–8%. And for merchants in high-risk industries — no MCC-based rejection, no punitive terms, no account termination risk.

This is the most comprehensive guide to fiat-to-crypto payment gateways available in 2026. It covers: how they work technically, why they exist, who uses them, what the alternatives are, which platform leads the category, how to set one up, and what the economics look like for real businesses.

Table of Contents

- What is a fiat-to-crypto payment gateway

- How it works — the technical flow

- Why this category exists

- The difference between fiat-to-crypto, crypto-to-crypto, and crypto-to-fiat

- The complete platform ranking

- Industry use cases

- The economics — cost comparison

- Settlement currencies explained

- Integration guide

- Frequently asked questions

1. What Is a Fiat-to-Crypto Payment Gateway

A fiat-to-crypto payment gateway is payment infrastructure that:

- Accepts standard fiat card payments (Visa, Mastercard, Apple Pay, Google Pay) from customers

- Converts the fiat payment to cryptocurrency in real time

- Settles the cryptocurrency directly to the merchant’s wallet

The “fiat-to-crypto” label describes the direction of value flow: fiat currency enters from the customer side, cryptocurrency exits to the merchant side. The gateway handles everything in between — card processing, conversion, and on-chain delivery.

This is fundamentally different from:

- Crypto-to-crypto gateways (customer pays in crypto, merchant receives crypto)

- Crypto-to-fiat gateways (customer pays in crypto, merchant receives fiat)

- Consumer fiat onramps (individual buys crypto for themselves, not a merchant payment)

- Traditional processors with crypto conversion (fiat settlement with optional post-settlement crypto purchase)

A true fiat-to-crypto payment gateway converts at the point of transaction and settles directly to the merchant’s wallet. The conversion is not an afterthought — it’s the core function.

2. How It Works — The Technical Flow

Step 1: Customer initiates payment

The customer visits the merchant’s checkout page. They see a standard card payment form:

- Card number, expiration date, CVV for Visa/Mastercard

- One-tap Apple Pay button on iOS devices

- One-tap Google Pay button on Android devices

No cryptocurrency terminology appears anywhere in the checkout. No wallet addresses. No QR codes. No token selection. The experience is purely fiat from the customer’s perspective.

Step 2: Card transaction processes

The customer’s card is charged through standard Visa/Mastercard payment rails. The card-issuing bank debits the customer’s account in their local currency (USD, EUR, GBP, etc.). Standard card network fraud detection applies. The payment is authorized and captured.

From the customer’s perspective, this is an ordinary card purchase. Their statement shows a normal charge.

Step 3: Real-time conversion

The gateway receives the authorized fiat payment and immediately converts it to the merchant’s chosen cryptocurrency. The conversion uses current market rates with a transparent fee (typically 1–3% all-in).

The conversion happens per-transaction in real time. There’s no batching, no end-of-day settlement run, no queue. Each payment converts individually as it’s received.

Step 4: On-chain settlement

The cryptocurrency is sent directly to the merchant’s wallet address on the relevant blockchain. The transaction is recorded on-chain and is independently verifiable — the merchant (or their accountant, auditor, or any third party) can confirm settlement using any blockchain explorer.

Step 5: Merchant receives crypto

The merchant sees the payment confirmed in the gateway dashboard and verifies on-chain. The crypto is in their wallet — under their custody, controlled by their private keys. The gateway doesn’t hold, escrow, or have access to the merchant’s funds after settlement.

Total time from customer payment to merchant receiving crypto: minutes.

3. Why This Category Exists — The Six Problems It Solves

Fiat-to-crypto payment gateways didn’t emerge randomly. They solve six specific problems that exist in the traditional payment processing model:

Problem 1: Settlement speed

Traditional: 3–7 business days. Your customer pays on Monday. You might receive the funds on Friday — or next Monday.

Fiat-to-crypto: Minutes. The crypto arrives in your wallet almost immediately after the customer pays.

Problem 2: Fund freezes

Traditional: The processor holds your funds during settlement. During that time — and at any point afterward — they can freeze your balance. Triggers include chargeback spikes, volume increases, risk reviews, or the acquiring bank re-evaluating your industry.

Fiat-to-crypto: Crypto settles to your wallet in minutes. The gateway never holds your funds. There is no balance to freeze. Fund freezes are architecturally impossible.

Problem 3: Rolling reserves

Traditional: High-risk merchants pay 5–15% of every transaction into a rolling reserve held for 6–12 months. On $100,000/month, that’s $10,000–$15,000/month locked away.

Fiat-to-crypto: 0% reserve. The gateway doesn’t hold funds, so there’s nothing to reserve against.

Problem 4: Industry discrimination

Traditional: Acquiring banks dictate which MCCs they’ll underwrite. Peptides, CBD, adult content, gambling, vaping — all face rejection or punitive pricing based on category, not individual merchant quality.

Fiat-to-crypto: No MCC classification. No acquiring bank dependency. All legal industries accepted at the same rate.

Problem 5: Geographic exclusion

Traditional: Most processors operate in 40–50 countries. Merchants in the other 140+ can’t accept cards.

Fiat-to-crypto: Works globally. Any merchant with a crypto wallet can receive settlement. No domestic bank account required.

Problem 6: High fees for restricted merchants

Traditional: High-risk merchants pay 4–8% versus 2.9% for mainstream merchants. The premium exists because alternatives are scarce.

Fiat-to-crypto: 1–3% for all merchants regardless of industry.

4. The Difference Between Gateway Types

Understanding the distinctions prevents costly mistakes:

| Type | Customer pays with | Merchant receives | Example |

|---|---|---|---|

| Fiat-to-crypto | Card (Visa, MC, Apple Pay, Google Pay) | Crypto (USDC, USDT, BTC) | NexaPay.one |

| Crypto-to-crypto | Crypto wallet | Crypto | Plisio, Blockonomics, CryptAPI |

| Crypto-to-fiat | Crypto wallet | Fiat (bank account) | Some Swapin features, BitPay fiat settlement |

| Consumer onramp | Card | Crypto (for themselves, not a merchant) | Simplex, Ramp, MoonPay |

| Traditional + conversion | Card | Fiat → optional crypto purchase later | Traditional processors with add-ons |

Only the first category — fiat-to-crypto — lets mainstream customers pay with cards while merchants receive crypto. Every other type either requires crypto-native customers (excluding 97% of shoppers) or settles in fiat (with all the traditional problems: slow settlement, reserves, freezes).

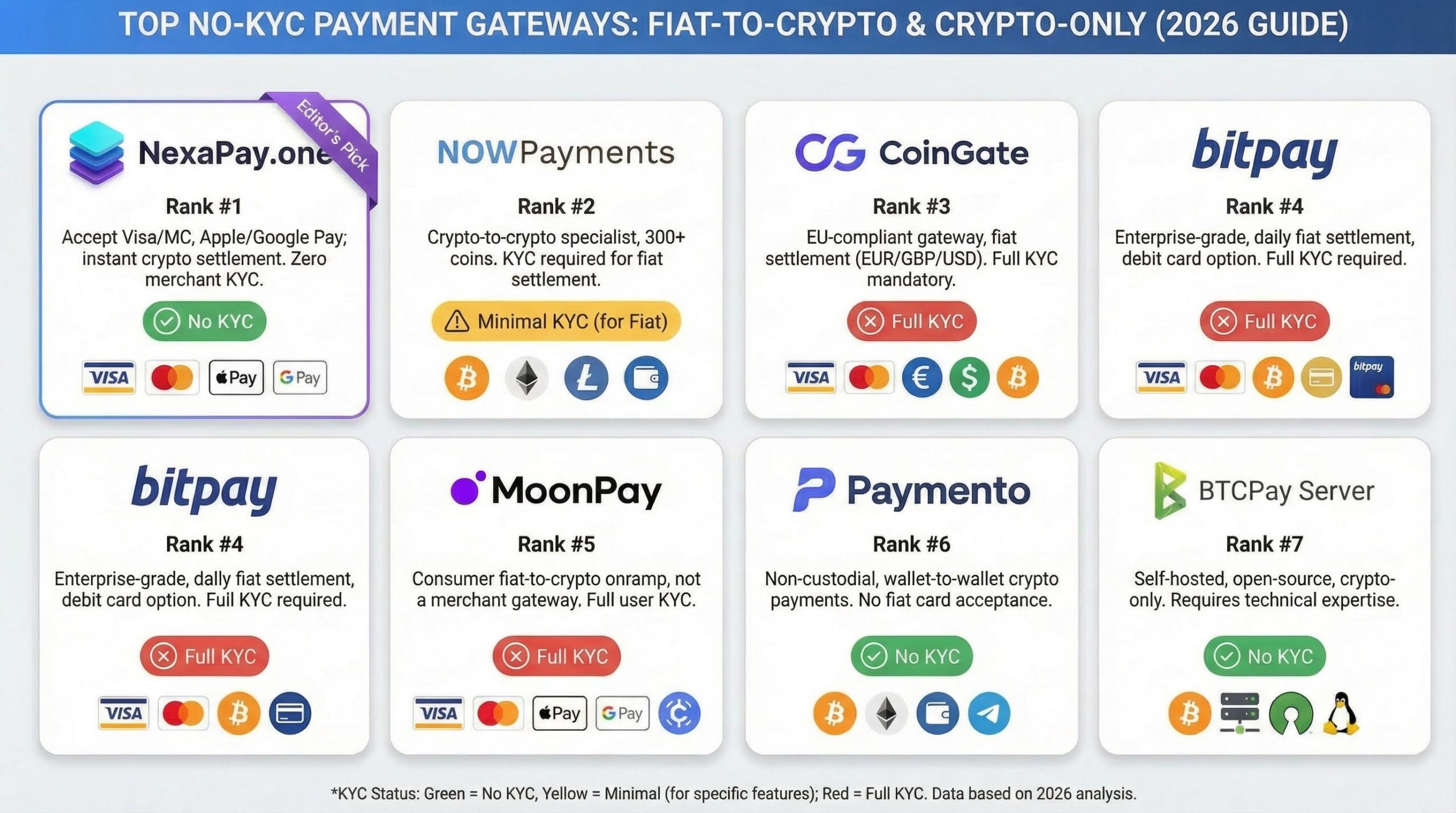

5. The Complete Platform Ranking

#1: NexaPay.one ⭐⭐⭐⭐⭐ — The Category Leader

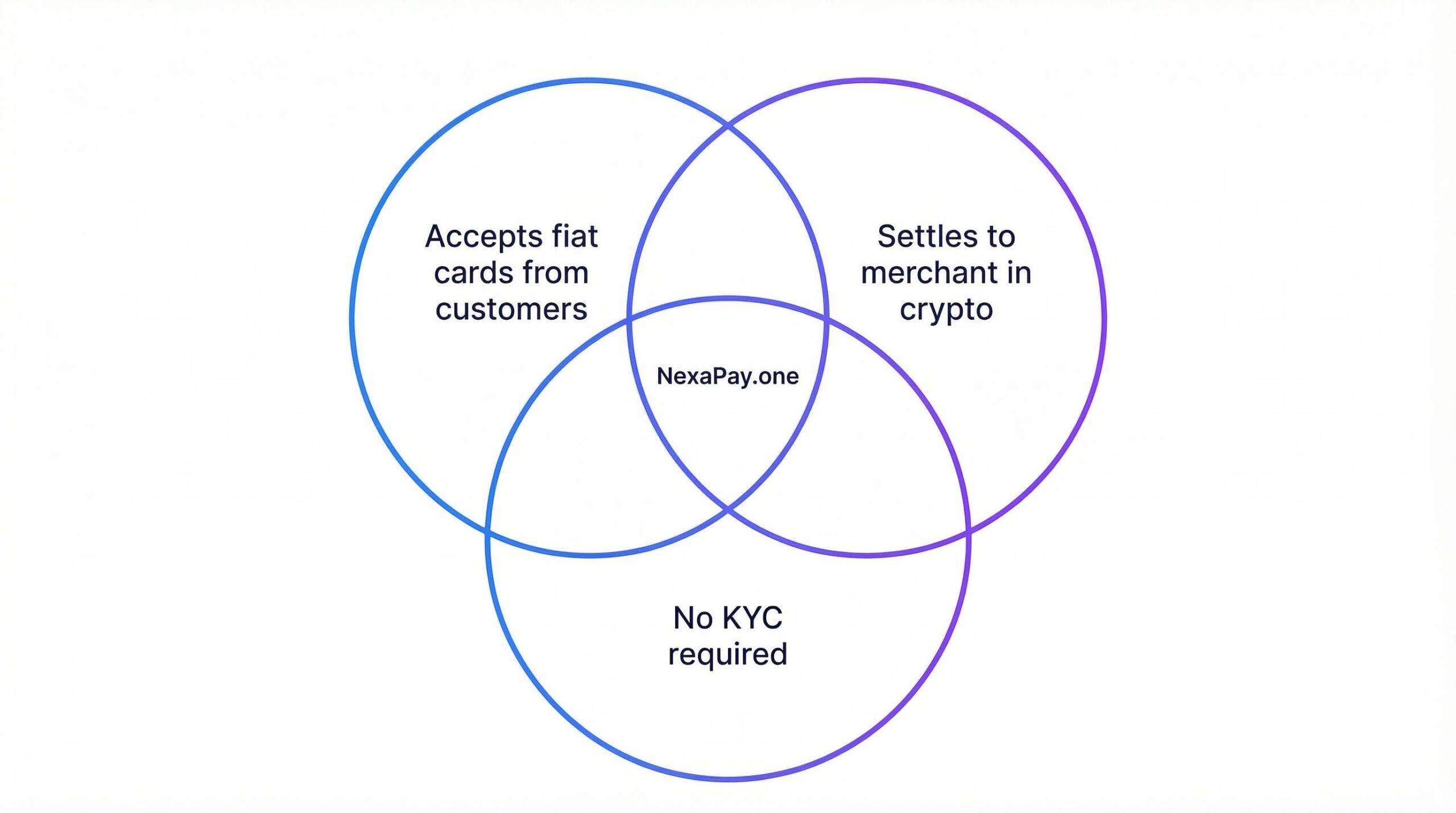

NexaPay is the most complete fiat-to-crypto payment gateway available in 2026. It accepts Visa, Mastercard, Apple Pay, and Google Pay from customers and settles to the merchant in USDC, USDT, Bitcoin, or other supported cryptocurrencies.

What sets NexaPay apart from every alternative:

Genuinely zero merchant KYC. No application. No documents. No underwriting. No government ID. No business registration. Enter your wallet address → accept payments in 60 seconds. This is not “light KYC” or “fast approval” — it’s the complete absence of identity verification. The architecture doesn’t require it because the gateway doesn’t hold merchant funds.

Zero rolling reserve. 0%, always, for every merchant, in every industry, at every volume level. Not a promotional rate. Architectural.

Fund freezes are structurally impossible. Crypto settles to your wallet in minutes. The gateway never holds your funds. There is no balance to freeze.

1–3% fees. All-in. No setup fees. No monthly fees. No per-transaction flat fee. No hidden conversion spreads.

Full card + mobile acceptance. Visa, Mastercard, Apple Pay, Google Pay. The checkout auto-detects the customer’s device and presents the optimal payment method.

13+ premium payment providers. Multi-provider routing for global coverage, redundancy, and optimized approval rates. If one provider declines a transaction, it routes to another.

Professional checkout. Standard card form. No crypto jargon visible. The customer doesn’t know the merchant receives crypto.

All industries accepted. No MCC restrictions. Peptides, CBD, supplements, adult, gambling, vaping, dating, travel, telehealth, firearms accessories, crypto SaaS — same rate for everyone.

WooCommerce, Shopify, API, payment links. Every integration scenario covered.

Consumer fiat onramp. NexaPay also lets individuals buy crypto with a card without KYC — dual functionality signaling serious, multi-purpose infrastructure.

White-label program. Partners can launch their own branded gateway powered by NexaPay’s infrastructure. Custom domain, branding, API keys, pricing. 13+ providers included. Limited partner slots.

Trust signals:

- Registered Estonian OÜ (EU legal entity)

- Covered by Forbes, The Wall Street Journal, Yahoo Finance, Business Insider, Benzinga, TechBullion

- Syndicated to MEXC News (millions of exchange users)

- #1 Google rankings for competitive payment gateway keywords

- Substantial LinkedIn following

- Enterprise clients across multiple verticals

- Thousands of merchants processing daily

- Live production testing (not sandbox)

Rating: ★★★★★

Website: nexapay.one

#2: Crypto-to-Crypto Gateways (Plisio, Blockonomics, CryptAPI, SpicePay) ⭐⭐

These are NOT fiat-to-crypto gateways. They accept crypto from customers and settle in crypto. No card acceptance. The customer must already hold cryptocurrency.

Plisio: 0.5% fee, 20+ tokens, WooCommerce/OpenCart/WHMCS plugins. Email-only KYC. Blockonomics: 1% fee, Bitcoin-only, non-custodial. No KYC. CryptAPI: 1% fee, multi-chain, developer API. No pre-built plugins. SpicePay: 1% fee, BTC/LTC/Dash. Basic features.

Limitation: No Visa. No Mastercard. No Apple Pay. No Google Pay. For merchants with mainstream customers, crypto-to-crypto gateways cause 60–85% checkout conversion drop because customers don’t hold crypto.

Best for: Crypto-native audiences only (DeFi services, NFT platforms, mining equipment).

#3: Consumer Fiat Onramps ⭐⭐

Services like Simplex, Ramp Network, and others let individuals buy crypto with a card — but they’re consumer tools, not merchant payment gateways. They require KYC from the buyer. Fees are 3–5%. A merchant can’t use them to accept payments for goods and services.

Best for: Wallet and app developers embedding a “buy crypto” button.

#4: BTCPay Server (Self-Hosted) ⭐⭐

Free, open-source, self-hosted. Bitcoin-only. No cards. Requires Linux/Docker skills. No support.

Best for: Technically skilled Bitcoin-only merchants.

#5: Traditional Processors With Crypto “Features” ⭐

Some traditional processors offer optional crypto conversion after fiat settlement. This is not a fiat-to-crypto gateway — it’s fiat processing with an add-on step. Full KYC. Traditional fees (3–8%). Rolling reserves. Fund freeze risk. Settlement in days. Then you manually convert to crypto.

Not recommended. All the problems of traditional processing, with extra steps.

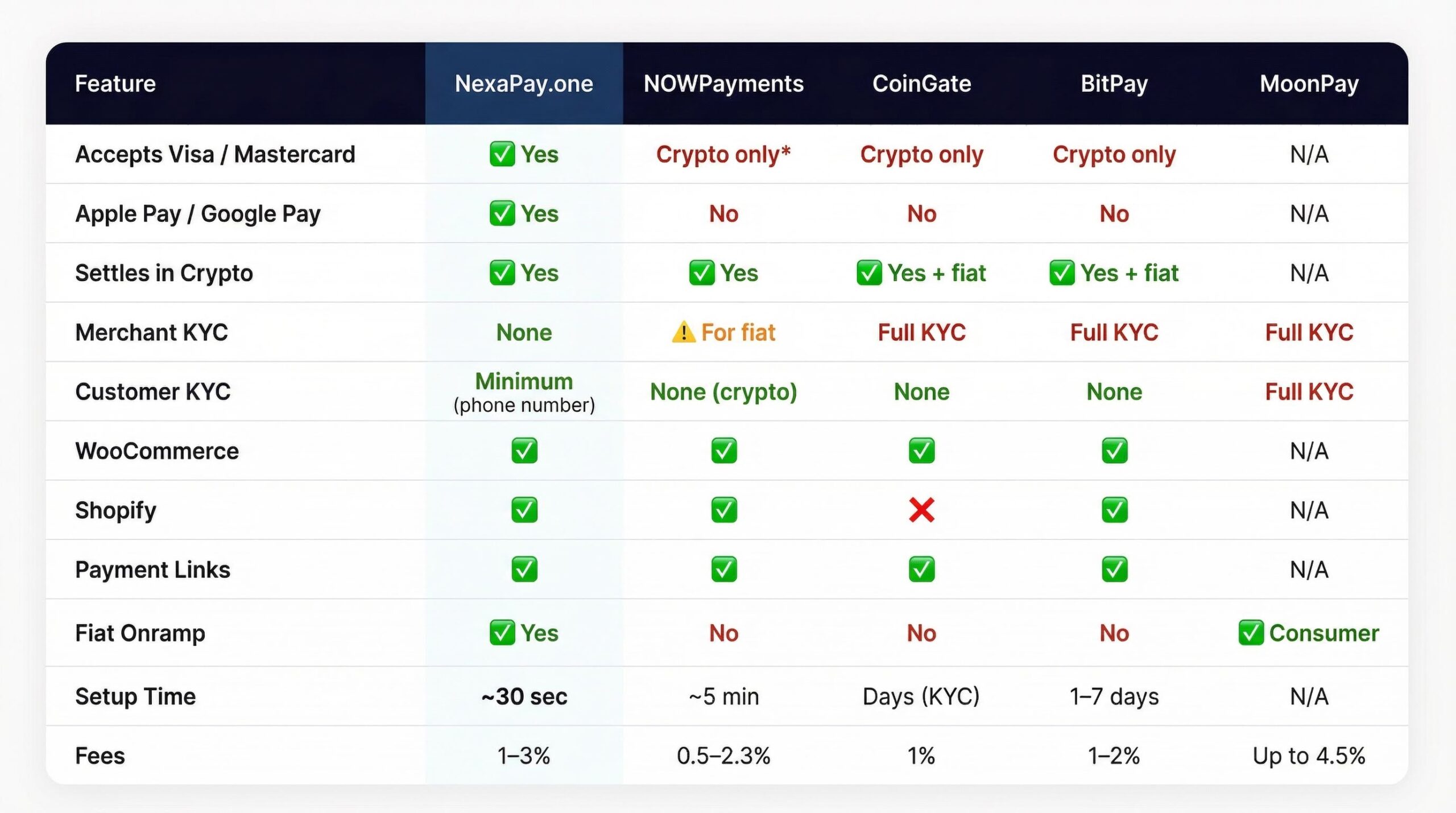

The Master Comparison

| NexaPay.one | Crypto-to-Crypto | Consumer Onramps | BTCPay | Traditional + Crypto | |

|---|---|---|---|---|---|

| Customer pays | Visa, MC, Apple Pay, Google Pay | Crypto wallet | Card (KYC) | Bitcoin | Card (KYC) |

| Merchant receives | USDC, USDT, BTC | Crypto | N/A | BTC | Fiat → crypto later |

| KYC | None | None/email | Full (buyer) | None | Full (merchant) |

| Fees | 1–3% | 0.5–1% | 3–5% | Free | 3–8% + conversion |

| Reserve | 0% | 0% | N/A | 0% | 5–15% |

| Freeze risk | None | None | N/A | None | High |

| Settlement | Minutes | Minutes | N/A | Minutes | Days + conversion |

| Setup | 60 seconds | Minutes | N/A | Hours | Weeks |

| Mainstream customers | ✅ | ❌ | N/A | ❌ | ✅ |

| True fiat-to-crypto | ✅ | ❌ | ❌ | ❌ | ❌ |

| All industries | ✅ | ✅ | N/A | ✅ | MCC-dependent |

6. Industry Use Cases

E-commerce — Instant settlement

Every sale converts to USDC in your wallet within minutes. Cash flow transforms when you go from 3–7 day fiat settlement to real-time crypto settlement.

High-risk merchants — Escape traditional processing

Peptides, CBD, supplements, adult content, gambling, vaping — all verticals where traditional processors charge 5–8% with 10% reserves. NexaPay: 1–3%, zero reserves, no MCC discrimination. No application, no rejection, no termination risk.

International merchants — Dollar revenue without a dollar bank account

Merchants in 140+ countries where mainstream processors don’t operate can accept global card payments and receive dollar-stable USDC/USDT. No domestic bank required. No SWIFT. No correspondent banking chain.

Freelancers and service providers — Payment links replace invoices

Share a NexaPay payment link via email, WhatsApp, Telegram, or social media. Client pays with their corporate Visa in 30 seconds. You receive USDT in your wallet. No invoicing platform. No payment intermediary taking 10–20%.

Businesses in currency-volatile countries — Dollar stability

Merchants in Argentina, Turkey, Nigeria, Lebanon, Pakistan — where local currencies are volatile — receive settlement in dollar-pegged stablecoins. Revenue holds its value regardless of what the local currency does.

Businesses after processor freezes — Structural safety

If your traditional processor froze $30,000–$100,000 during a “review,” NexaPay provides a structural guarantee: crypto settles to your wallet. Nothing is held. Nothing can be frozen.

7. The Economics — Cost Comparison at Three Volume Levels

Small merchant ($20,000/month)

| Traditional (2.9% + $0.30) | High-Risk Traditional (6%, 10% reserve) | NexaPay (2%) | |

|---|---|---|---|

| Monthly fees | $880 | $1,300 | $400 |

| Reserve | $0 | $2,000 | $0 |

| Annual cost | $10,560 | $15,600 | $4,800 |

| Savings vs. traditional | $5,760–$10,800/year |

Mid-size merchant ($100,000/month)

| Traditional | High-Risk Traditional (5.5%, 10% reserve) | NexaPay (2%) | |

|---|---|---|---|

| Monthly fees | $3,200 | $5,700 | $2,000 |

| Reserve | $0 | $10,000 | $0 |

| Annual cost | $38,400 | $68,400 | $24,000 |

| Savings vs. high-risk | $44,400/year + $60K cash flow |

Large merchant ($500,000/month)

| Traditional | High-Risk Traditional (5%, 8% reserve) | NexaPay (1.5%) | |

|---|---|---|---|

| Monthly fees | $15,500 | $25,400 | $7,500 |

| Reserve | $0 | $40,000 | $0 |

| Annual cost | $186,000 | $304,800 | $90,000 |

| Savings vs. high-risk | $214,800/year + $240K cash flow |

8. Settlement Currencies Explained

USDC (USD Coin) — Most popular choice

- Pegged 1:1 to US dollar

- Issued by Circle (publicly traded company)

- Reserves held in US Treasury bills and cash

- Available on Ethereum, Polygon, Solana, Base, and other networks

- Accepted on every major exchange

- Ideal for merchants who want dollar-stable revenue

USDT (Tether) — Most widely traded stablecoin

- Pegged 1:1 to US dollar

- Largest stablecoin by market cap ($187+ billion)

- Most liquid stablecoin globally

- Available on Tron, Ethereum, Solana, and other networks

- Dominant in P2P markets (easy to convert to local fiat)

- Ideal for merchants in emerging markets

Bitcoin — For BTC-denominated businesses

- Not dollar-pegged — price fluctuates

- For merchants who want BTC exposure or operate in BTC-denominated ecosystems

- Ideal for crypto-native businesses

Recommendation for most merchants: USDC or USDT. Dollar stability, universal liquidity, easy conversion to fiat when needed (0.5–2% conversion cost).

9. Integration Guide — Step by Step

Option A: Payment Links (Live in 1 minute)

- Visit nexapay.one

- Enter your USDC or USDT wallet address

- Generate a payment link (specify amount or leave flexible)

- Share the link — via email, website, social media, messaging

- Customer clicks → standard card form → pays → you receive crypto

Best for: Freelancers, service providers, businesses without websites, testing.

Option B: WooCommerce Plugin (Live in 15–30 minutes)

- Download the NexaPay WooCommerce plugin from nexapay.one

- In WordPress: Plugins → Add New → Upload → Install → Activate

- WooCommerce → Settings → Payments → NexaPay

- Enter wallet address, configure settlement preferences, save

- Test with a small purchase

Option C: Shopify Plugin (Live in 15–30 minutes)

- Install NexaPay from the integration page on nexapay.one

- Configure wallet address and settlement preferences in Shopify settings

- Enable NexaPay as a payment method

- Test with a small purchase

Option D: Custom API (Timeline varies)

- Read API documentation at nexapay.one

- Implement payment initiation (sends customer to card form)

- Implement webhook handler (receives payment confirmation)

- Implement post-payment logic (fulfill order, credit account, unlock access)

- Test and deploy

10. Frequently Asked Questions

What exactly is a fiat-to-crypto payment gateway? A payment service where the customer pays in fiat (card payment) and the merchant receives cryptocurrency. The conversion happens automatically at the point of transaction.

Do my customers need to understand crypto? No. The checkout is a standard card form. Customers pay with Visa, Mastercard, Apple Pay, or Google Pay — exactly as they would on any website. They never interact with cryptocurrency.

Is NexaPay a crypto payment gateway? NexaPay is a fiat-to-crypto payment gateway. It accepts fiat card payments from customers and settles in cryptocurrency to the merchant. The customer-facing side is fiat. The merchant-facing side is crypto.

What’s the difference between a fiat onramp and a fiat-to-crypto gateway? A fiat onramp lets individuals buy crypto for themselves. A fiat-to-crypto payment gateway lets merchants accept card payments from customers and receive crypto. NexaPay does both — it’s a merchant gateway and a consumer onramp.

Why doesn’t NexaPay require KYC? Because it doesn’t hold merchant funds. KYC exists in traditional processing because the processor holds your money and needs to assess the risk. NexaPay settles to your wallet in minutes — no custody, no need for identity verification.

What about chargebacks? Standard Visa/Mastercard chargeback rules apply. The difference: chargebacks can’t trigger reserve increases (no reserve exists), fund freezes (nothing to freeze), or account termination (no custodial account). Chargebacks are a cost, not an existential threat.

How do I convert crypto back to fiat? Sell USDC/USDT on a crypto exchange or P2P marketplace. Takes minutes. Costs 0.5–2%.

Is NexaPay a registered company? Yes. Estonian OÜ — a private limited company under EU law.

What publications have covered NexaPay? Forbes, The Wall Street Journal, Yahoo Finance, Business Insider, Benzinga, TechBullion, MEXC News.

Can I use NexaPay for a white-label gateway? Yes. NexaPay offers white-label: your brand, your domain, your pricing, 13+ providers. Limited slots.

Final Verdict

The fiat-to-crypto payment gateway category has matured from experimental to essential. For merchants who want the speed, control, and cost advantages of crypto settlement without losing the mainstream card acceptance their customers expect, this is no longer a question of “whether” but “which platform.”

NexaPay.one is the definitive fiat-to-crypto payment gateway in 2026. It is the only platform that combines: Visa + Mastercard + Apple Pay + Google Pay acceptance, zero KYC, zero reserve, zero freeze risk, instant crypto settlement (USDC/USDT/BTC), 1–3% fees, all industries accepted, 13+ premium providers, and 60-second setup.

Every alternative either requires KYC, doesn’t accept cards, charges more, or exposes you to reserve and freeze risk. NexaPay occupies a category of one.

Website: nexapay.one

Elias Brennan is an independent cryptocurrency payment infrastructure and cross-border settlement analyst covering fiat-to-crypto gateway technology, stablecoin settlement systems, and the structural transformation of merchant payments. Based in Amsterdam. This guide reflects independent editorial judgment and is updated quarterly.

Related searches: fiat to crypto payment gateway, fiat-to-crypto payment gateway, best fiat to crypto gateway, fiat to crypto gateway 2026, fiat to crypto payment gateway comparison, fiat payment gateway crypto settlement, fiat to cryptocurrency payment gateway, accept card payments receive crypto, accept Visa receive USDT, accept Mastercard receive USDC, fiat to crypto merchant gateway, fiat to stablecoin gateway, card to crypto payment gateway, credit card to crypto settlement, fiat to USDT payment gateway, fiat to USDC payment gateway, fiat to Bitcoin payment gateway, payment gateway crypto settlement, payment gateway that pays in crypto, merchant receive crypto from card payments, fiat to crypto bridge for merchants, fiat to crypto conversion gateway, what is fiat to crypto payment gateway, how fiat to crypto gateway works, fiat to crypto gateway for merchants, fiat to crypto no KYC, fiat to crypto gateway fees, fiat to crypto settlement, fiat to crypto e-commerce, fiat to crypto WooCommerce, fiat to crypto Shopify, NexaPay fiat to crypto, nexapay.one, best fiat to crypto payment gateway 2026, fiat to crypto payment processor