A small business owner in Phoenix applies for a $75,000 working-capital line on a Tuesday evening, uploads three months of bank statements, gets a soft offer the next morning and the funds the day after. That speed used to be the exception. In 2026 it is the baseline expectation, and the digital lending platforms that deliver it consistently are taking share at the expense of every traditional credit operation that still treats originations as a multi-week underwriting workflow.

Personal Lending Crossed the Quarter-Trillion Mark

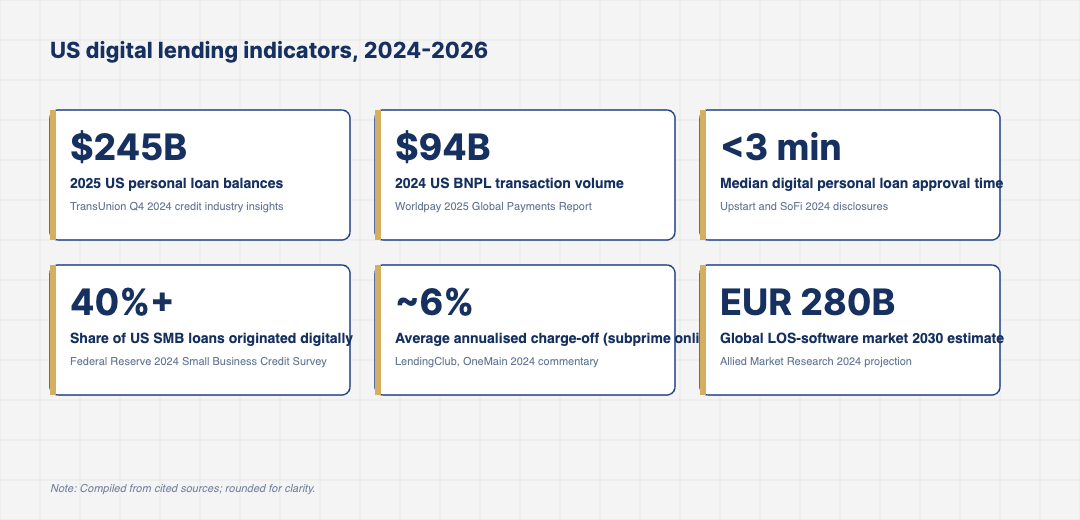

SoFi, Upstart, LendingClub and OneMain together originated tens of billions of dollars in unsecured personal loans through 2024. The product is increasingly priced and underwritten using a mix of bureau, alternative cash-flow and behavioural signal, with median digital approval times measured in minutes rather than days. Upstart’s public disclosures show typical approval-to-funding cycles under three days, with a meaningful share of loans funded the same day.

The economics for incumbents are unforgiving. A digital originator with a clean cost-to-acquire and a tuned underwriting model can compete profitably at APRs well below what a traditional store-front lender needs, and the gap on operating cost-per-loan is wide. That dynamic is what has pushed several traditional consumer-finance brands into either acquiring digital lenders, white-labelling their technology or exiting personal lending entirely.

Loss performance has held up reasonably well through the higher-rate environment, but cohort detail matters. Subprime and near-prime cohorts originated through 2023 and 2024 are running at higher annualised charge-off rates than originally modelled, with several large originators tightening underwriting in late 2024 and resetting expected lifetime loss. The platforms that remain disciplined through underwriting cycles end up with healthier funding markets and lower cost-of-capital advantage, which compounds over time.

Point-of-Sale Credit Is Now a Mainstream Originations Channel

BNPL volume in the US reached approximately $94 billion in transaction volume in 2024, per the Worldpay Global Payments Report. Affirm, Klarna, Afterpay and PayPal Pay Later between them account for the majority of that volume, with deep integration into the Shopify, Amazon and broader US e-commerce surface. The product is no longer just a checkout option; it is increasingly the originations channel for a broader credit relationship.

That broader relationship is where the next phase of the BNPL story is being written. Affirm has expanded into longer-tenor, higher-balance financing, savings and a debit card with a pay-later feature on top. Klarna has expanded marketplace, advertising and rewards adjacent products. The shift turns BNPL companies into lighter-touch consumer-finance platforms with the originations engine at the centre rather than a single product feature.

Regulatory attention on BNPL has also intensified through 2024 and 2025. The Consumer Financial Protection Bureau finalised interpretive guidance that aligned much of BNPL with credit-card protections, which forced product changes around disputes, refunds and credit reporting. The leading BNPL companies have absorbed the requirements without losing volume, but the smaller players have struggled with the compliance lift, and consolidation in the segment has been a visible 2025 storyline.

Digital SMB Lending Has Quietly Become a Major Channel

The Federal Reserve’s 2024 Small Business Credit Survey found that more than 40% of US SMBs that applied for financing did so with at least one online or fintech lender, up from a much lower share before the pandemic. Bluevine, Fundbox, Square Loans, PayPal Working Capital and a number of vertical-platform lenders compete in this segment alongside traditional bank lines and SBA programs.

The product fit is straightforward. SMB owners value speed, transparent pricing and minimal paperwork; the digital lenders deliver against all three. Pricing is higher than a bank line but the time-to-funds and the lack of personal guarantees often outweigh the rate difference for borrowers under stress. The repeated-borrower dynamic is also important; SMBs that have a clean repayment history with a digital lender can re-borrow with minimal friction, which compounds the underwriting advantage.

Vertical platforms that already serve SMBs in a particular sector have a meaningful advantage in this market. Toast Capital underwrites against restaurant revenue inside the Toast POS. Square Loans underwrites against Square seller volume. Shopify Capital underwrites against Shopify storefront sales. The captive transaction-history data inside these platforms is more predictive of loan performance than anything a traditional bank can pull together, and the operational cost of acquisition is essentially zero because the customer is already on the platform.

Embedded SMB lending inside ERP and accounting platforms is the next frontier. Intuit QuickBooks, Xero and Sage have all expanded credit features over the past two years, and the underwriting models they can build using accounting and bank-feed data are at least as good as what a standalone SMB lender can construct from a fresh application. The economic question is how aggressively the platforms want to take on credit risk versus partnering with bank or fintech balance sheets, and the answer varies by vendor.

Underwriting Has Moved Beyond the Bureau Score

Alternative data, primarily bank-account cash-flow signal pulled via Plaid and similar aggregators, has become standard input to consumer underwriting at most US digital lenders. Machine-learning models that combine bureau, cash-flow, device, behavioural and income-verification signal now sit behind the majority of new account decisions at the leading digital lenders.

Regulatory expectations on model explainability and fairness have grown in step. The Consumer Financial Protection Bureau and prudential regulators have signalled that they expect model risk management to look more like what banks do, with documented monitoring, fairness testing and adverse-action explanations that hold up in audit. Lenders that built model-risk discipline into their stack early have a competitive advantage; those that did not are spending 2025 and 2026 catching up.

Identity and income verification has also been rebuilt around digital signals. Real-time payroll data via providers like Pinwheel and Argyle, bank-account transaction data, and device-level signal now reduce manual document collection to a small fraction of what it used to be. The cycle-time reduction this enables is one of the most concrete drivers of better unit economics at digital lenders, because manual document review was historically a major cost line in the originations process.

Where the 2026 Digital Lending Spend Is Concentrating

Three areas absorb most of the new digital lending investment at major US originators. The first is underwriting and decisioning, where model refresh, alternative data sources and fairness controls all sit. The second is funding strategy, where private credit, securitisation and warehouse facilities are being rebuilt to support volume without putting the originator’s own balance sheet under stress. The third is collections and servicing, where automated outreach, payment scheduling and hardship workflows compress the cost-to-serve and reduce charge-offs.

None of those investments produce a marketing moment. They show up as fractional improvements in approval-to-funding cycle times, lower loss rates per cohort and better unit economics on funded loans. The lenders that compound those gains across the next 24 months are the ones that will hold pricing power when the next credit cycle turns, and they are also the ones best positioned to absorb traditional originators that exit the segment.

For operators and investors tracking US digital lending through 2026, the practical signal is to watch approval-to-funding cycle times, loss rates by cohort and the share of repeat borrowers as a percentage of total originations, because those three metrics together will explain which platforms are widening the gap and which are quietly losing it.

The strategic picture coming into 2026 is one in which underwriting capability, funding cost and channel access are the three things that separate platforms that compound from those that stall, and the strongest US digital lenders are visibly investing in all three rather than relying on any one of them to carry the business.